Ratings Methodology for Small Business Loans

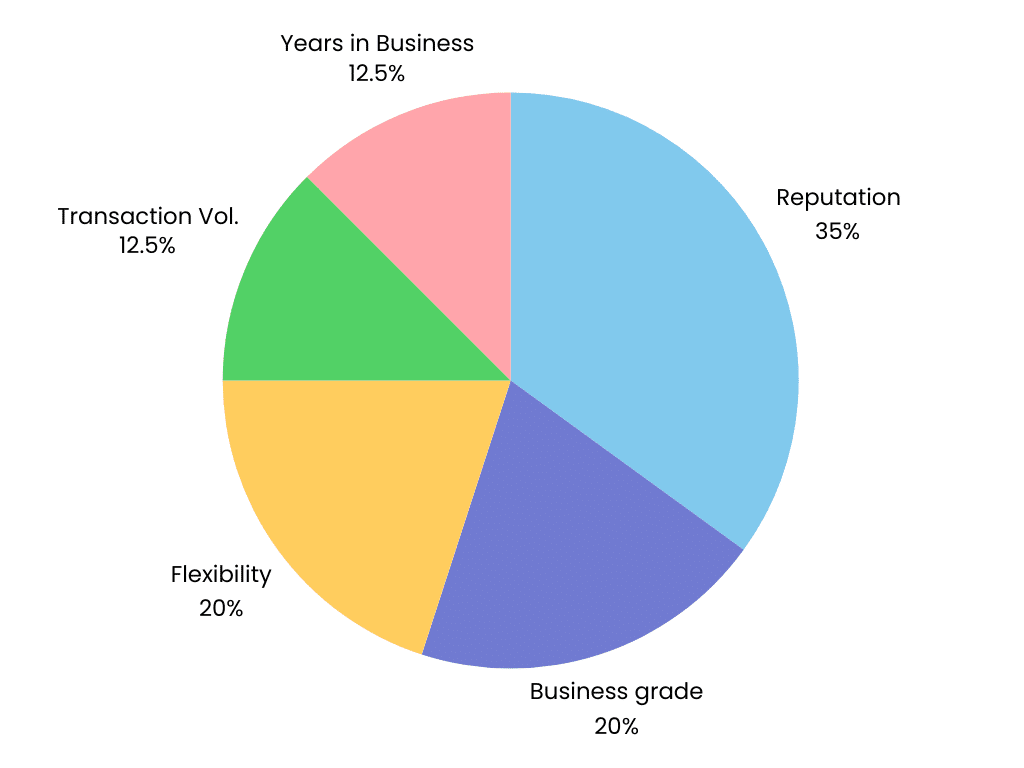

Market Shepherd's overall ratings for small business loans are evaluated against five major categories. A raw score is produced for each of the following:

- Reputation/Public Reviews: 35%

- Business grade: 20%

- Flexibility: 20%

- Transaction volume: 12.5%

- Years in business: 12.5%

Data collection and review process

Market Shepherd reviewed five of the most popular small business loans

based on online search volume. Some of these companies are MS partners, but this does not influence the review process.

We collect information from the lenders

and verify it through interviews and on company websites. We also use public review sites and business data collectors/providers.

Then, we rate the companies

on a scale of 1 to 5 on the following criteria: reputation, business grade, flexibility, transaction volume, and years in business. Each category constitutes a portion of the lender’s overall score. These scores generate ratings from 1 star (poor) to 5 stars (excellent). We then use the weighted categories to calculate a score for each lender. We divide that score by 5 and multiply it by 10 for our final score.

The review team

MS selects partners based on the findings of our independent reviewers. MS does not publish reviews or assessments at the direction of any company and our partners cannot pay us for a favorable review or rating. If you have any questions about a company mentioned on our site, including our partners, feel free to contact us.

Reputation/Public Reviews (35%)

This category is determined by public reviews. A public reviews rating between 4.5 and 5 equals a category score of 5, 4 through 4.5 equals 4, 3.5 through 4 equals 3, 3 through 3.5 equals 2, and anything less than 3 equals 1. This gives us a final score between 1 and 5.

Business grade (20%)

This category is derived from a business analysis conducted by the go-to-site for official business complaints. It takes into account each company’s grade and the presence or absence of accreditation. We start each company at a score from 1 to 5 based on their letter grade: 5 for A+, 4 for A, 3 for A-, 2 for B+, and 1 for B or less. Then we subtract 1 point for the absence of accreditation. This gives us a final score between 1 and 5.

Flexibility (20%)

This category takes into consideration the number of partners in the lender’s network and whether or not they are a direct lender. We start each company at a score of 5 and subtract 1 point for no direct lending and a partner network of less than 75 (or if not disclosed). This gives us a final score between 1 and 5.

Transaction Volume (12.5%)

This category evaluates the number of transactions each lender has completed. A transaction volume of 20,000+ equals a category score of 5, 15,000-19,999 equals 4, 10,000-14,999 equals 3, 5,000-9,000 equals 2, and 0-4,999 equals 1. This gives us a final score between 1 and 5.

Years in Business (12.5%)

This category looks at the number of years each lender has been in business. 10+ years equals a category score of 5, 8-9 equals 4, 6-7 equals 3, 4-5 equals 2, and 0-3 equals 1. This gives us a final score between 1 and 5.

Discretionary (not weighted)

A lender that provides a unique, small-business-friendly feature not commonly found among competitors may receive a higher score. Conversely, a lender could be rated lower if it has faced government regulatory actions in the past five years or has been credibly accused of predatory business lending practices.

If you have any feedback or questions, please don’t hesitate to contact us at info@marketshepherd.com.